Why Financial Systems Work Better Than Willpower

Many people approach money management with the best intentions. They promise themselves they will spend less, save more, and keep track of every expense. For a few weeks, the plan might work. But eventually life becomes busy, expenses pop up, and financial decisions start happening on autopilot again.

The challenge is not always discipline. Often the real issue is structure. When finances rely entirely on daily decision making, it becomes easy for emotions, stress, or convenience to influence spending.

Designing finances like a system changes this dynamic. Instead of constantly reacting to expenses, individuals create a framework that automatically directs income toward specific goals. In some cases, this shift in structure may even accompany broader financial adjustments, such as exploring options offered by debt negotiation companies while restructuring financial priorities.

When finances operate like a system rather than a series of individual decisions, consistency becomes much easier to maintain.

Thinking of Money Like Infrastructure

One helpful way to understand financial systems is to compare them with infrastructure. Roads, electricity networks, and water systems are designed to function reliably in the background. Once they are built correctly, they require far less daily attention.

Financial systems can function the same way. Instead of deciding where money should go every time income arrives, individuals design a structure that automatically distributes funds into specific categories. In a similar way, large investment platforms such as https://www.graniteasia.com/, apply structured financial frameworks to help manage and allocate capital efficiently.

For example, income might flow into one central account before being automatically transferred into separate accounts for essential expenses, savings, and discretionary spending.

This approach reduces decision fatigue because the system itself performs most of the work. People spend less time debating individual purchases and more time focusing on long term financial progress.

Educational resources from the Consumer Financial Protection Bureau budgeting and financial planning tools often highlight the benefits of structured financial planning systems for reducing stress and improving consistency.

Systems transform financial management from constant effort into sustainable structure.

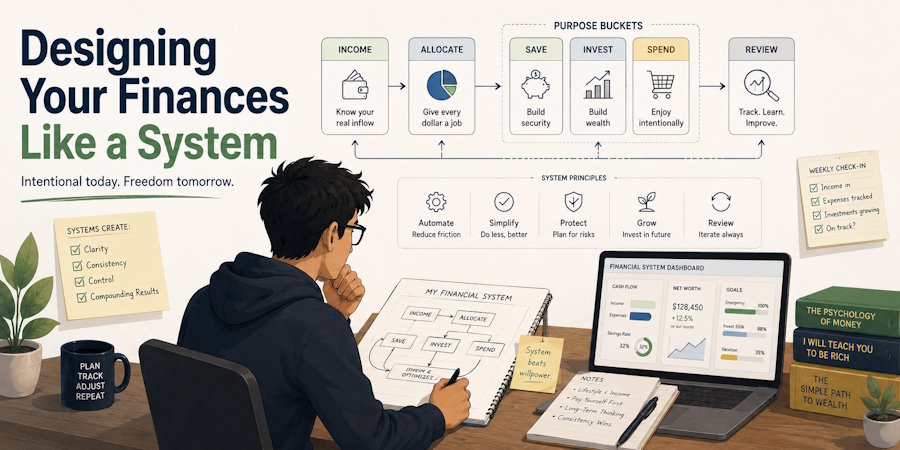

Using Financial Buckets to Organize Income

One of the most practical strategies for building a financial system involves using separate “buckets” for different financial purposes. Each bucket represents a category of spending or saving.

A common structure might include categories such as housing, transportation, savings, emergency funds, and personal spending. When income arrives, it is divided among these buckets according to predetermined percentages or amounts.

This structure helps individuals see clearly where their money is intended to go before spending decisions occur.

For example, if a specific account is designated for discretionary spending, individuals can enjoy those purchases without worrying about whether they are affecting essential expenses.

Financial buckets remove uncertainty by giving each dollar a clear destination.

Automation Reduces Emotional Decisions

Another important feature of financial systems is automation. Automated transfers and payments ensure that financial goals receive attention even during busy or stressful periods.

Automation might include setting up recurring transfers to savings accounts, scheduling automatic bill payments, or allocating funds toward investments each month.

These automated actions eliminate many of the emotional decisions that can interfere with financial plans. Instead of debating whether to save money this month, the system handles the decision automatically.

Automation also protects financial goals during periods when motivation is low. Because the system continues operating in the background, progress continues without requiring constant attention.

Over time, automation transforms good intentions into consistent habits.

Systems Provide Clarity During Financial Stress

Financial stress often arises when individuals feel uncertain about where their money is going or whether they can manage upcoming expenses.

A well-designed financial system provides clarity during these moments. When income is already organized into structured categories, individuals can quickly evaluate their situation.

They can see how much is allocated for essential costs, how much is available for discretionary spending, and how their savings are progressing.

This clarity makes it easier to make thoughtful decisions during challenging periods.

Guidance from the Federal Trade Commission consumer financial education resources emphasizes the importance of structured planning and financial awareness in maintaining long term financial stability.

Systems create a framework that supports thoughtful decisions rather than reactive ones.

Adjusting the System as Life Changes

Although financial systems provide structure, they should remain flexible enough to evolve as life circumstances change.

Income levels may increase or decrease. New goals may emerge, such as purchasing a home, starting a business, or funding education. Unexpected expenses may also require temporary adjustments.

Because financial systems are built from categories and automated flows, they can usually be modified without rebuilding the entire structure.

For example, adjusting the percentage of income directed toward savings or discretionary spending may be enough to accommodate new priorities.

Flexibility ensures that financial systems remain relevant rather than rigid.

Designing Systems That Support Long Term Goals

One of the greatest advantages of designing finances like a system is that it aligns everyday decisions with long term objectives.

When savings, investments, and essential expenses are built into the system itself, individuals no longer rely entirely on willpower to stay on track.

Each paycheck becomes an opportunity to reinforce financial priorities automatically.

This approach also reduces the mental load associated with financial management. Instead of constantly evaluating each purchase, individuals can trust the structure they have created.

Over time, the system quietly supports progress toward larger financial goals.

Building Stability Through Structure

Designing finances like a system changes the relationship people have with money. Instead of feeling reactive or uncertain, individuals gain a sense of control through clear structure.

Financial buckets organize income into purposeful categories. Automation ensures that important goals receive consistent attention. Flexible adjustments allow the system to evolve alongside changing circumstances.

The result is a financial environment where progress happens steadily in the background.

Rather than relying on perfect discipline, individuals rely on thoughtful design. And when finances are designed like a system, the path toward stability becomes far easier to follow.